More from our experts

Learning how to set up direct deposit for employees can be a smart move for businesses because it’s one of the easiest and most popular ways to pay workers and can put less stress on an employer’s resources.

Key takeaways on how to set up direct deposit

- Direct deposit is a way to electronically transfers wages directly into an employee’s bank account

- Setup requires a company bank account, payroll provider, employee authorization, and an employee’s bank account number to distribute funds

- Over 90% of U.S. employees receive their paychecks through direct deposit

- Direct deposit is generally easier and safer than other payment methods because it reduces the risk of theft, loss of checks, and input errors.

Though direct deposit is a common payment method, if you are using it for the first time to pay employees, it can feel like there are a lot of moving parts that need to be managed. However, once you understand the basics, the setup should be straightforward.

In this guide, we explain how this payment method works, how to set it up without issues, and what to keep in mind when using it in your organization.

What direct deposit is

Simply put, direct deposit is an electronic payment method that transfers funds from an employer’s bank account directly into an employee’s bank account when processing payroll. It eliminates the need for physical paychecks and manual distribution, though companies can still issue paper checks if needed.

This process is a type of electronic funds transfer (EFT), but “direct deposit” is the term most employees are more likely to be familiar with.

ACH

If you are getting familiar with direct deposit (or payroll processing in general), an acronym that’s bound to come up is ACH.

This stands for automated clearing house, a system of over 10,000 banks and financial institutions that use a “batch” system to transfer funds electronically from one bank to another. Direct deposit uses this system to pay employees quickly and efficiently. This is important to point out since it is a major part of how money gets sent from the employer to the employee.

Now that we have a description of this payment type, let’s get some details on how this process gets going.

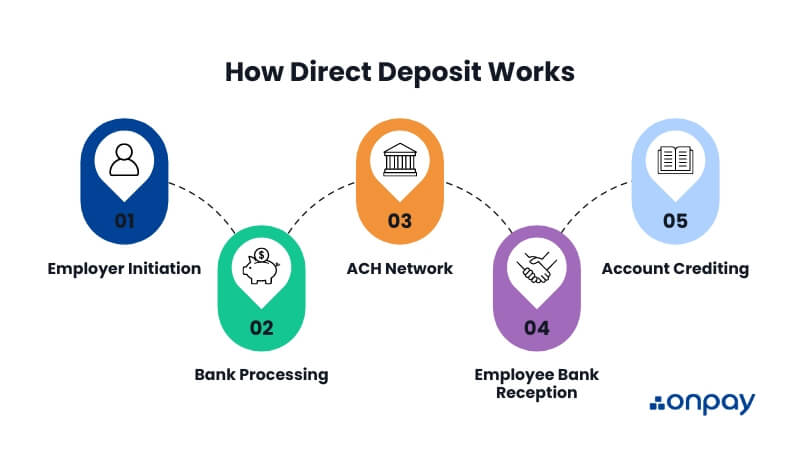

Understanding how direct deposit payroll works

While we’ll delve into the setup process further in the article, you might be wondering what is actually happening to move wages from point A (the employer’s bank account) to point B (the employee’s bank account). Here’s an overview.

- Employer initiation: The process begins when an employer submits a payment instruction to their bank.

- Bank processing: The employer’s bank receives the direct deposit orders and groups them into batches. These batches are then sent to the Automated Clearing House (ACH) network at various intervals throughout the day.

- ACH network: The ACH, a centralized system that coordinates electronic transfers between financial institutions, processes these batches and is responsible for routing the funds to the appropriate employee banks.

- Employee bank reception: The banks where employees hold their accounts receive the transfer instructions from the ACH.

- Account crediting: The employees’ banks then credit the designated accounts with the specified amounts. On the flip side, the employer’s account is debited for the total amount of the payroll that’s being paid.

This electronic process eliminates the need for paper checks and manual deposits, making it faster and more efficient for both employers and employees.

Now that we better understand how money moves from one location to another with direct deposit, let’s find out how to set it up.

How do I set up direct deposit for my company?

Setting up direct deposit might sound like a headache at first, but below are some steps that can make this process painless.

Having a payroll provider is paramount

Before you can get direct deposit up and running, you’ll need to decide which services company you are going to pay employees through. This is because you’ll need an organization to keep all of your employees and business information housed.

Whoever you choose will also be the ones responsible for pushing the funds to the ACH, who then batches the payments, disperses them to the banks, and ultimately into the accounts of workers. So what are the options?

- On one hand, you can work with payroll software companies like OnPay, who offer direct deposit as a feature and can set this up for you. Some HR software providers can help too.

- Chances are, the bank you have your business account with can also help get a direct deposit system in place.

Verify your bank account

Because funds will be moving from your company’s account to that of employees, the data will need to be verified. In many cases, the organization that wants to set up electronic funds transfer (and the primary signer of agreements at the company) is required to undergo a risk assessment. Once you have chosen a provider, they should initiate the risk assessment with the ACH they work with.

Collect data for direct deposit

In most cases, the information that you’ll need employees to provide is:

- Bank account number: an employee’s bank account number is a unique identifier for their specific account at their financial institution. For direct deposit, employees must provide this number to their employer so that payroll funds can be accurately deposited into their personal account.

- Bank routing number: this is a nine-digit code that identifies the financial institution where an employee’s bank account is held. It’s used along with the employee’s account number, to ensure that payroll funds are correctly transferred to the employee’s specific account.

- Account type the employee wants to use (generally a checking or savings account).

- Authorization form signed by the employee (That’s a fancy way of saying they are giving you permission to move funds from your employer account directly into their bank account)

We mentioned that you can use a software platform to set this up too, because many offer employee self-service portals so workers can have access and upload their info. This means they can set this up their account, agree to authorizations, and enter their personal and bank information on their own.

Does your pay schedule align with requirements?

Before implementing, confirm with your bank or payroll service provider that your existing pay schedule is going to be compatible with direct deposit. Paying wages this way involves a process where funds move out of from your account and through a clearing house before reaching employee bank accounts.

This system operates on preset days, so it’s worthwhile to factor in processing times and potential disruptions. You may need to adjust your pay schedule to accommodate:

- ACH processing times (typically 2-3 business days)

- Bank holidays (like federal holidays, for example)

- Weekends

Test run

Once you are certain your pay schedule is synced correctly, you’ll want to check with your bank or the online payroll provider to ensure you are safe to start running payroll. Be sure you know the date that employees can expect to receive wages in their bank account and communicate this day to them.

What does direct deposit cost?

Software companies generally charge either an initial direct deposit set-up fee, a monthly fee, or a fee per payroll run, or all three. Initial set-up fees can vary from $0 to $75 or more. Monthly costs can vary significantly, as well, with costs ranging from $40 a month to $60 per month or even more. Payroll providers also charge a per-employee fee each time you run payroll, which generally costs around $6 per employee. Finally, direct deposit fees generally range from $0.70 to $1.30 per deposit (depending on deposit volume).

Banks typically charge a setup fee too, ranging from $50 to $149 on average, according to the National Federation of Independent Business (NFIB). Some banks charge ongoing monthly fees for direct deposit, but most do not. Additionally, some banks charge various transaction fees depending on the number of employees on staff, so it pays to look at the fine print.

Related resource

Direct deposit pros and cons to consider

Employer advantages

Direct deposit is a proven payment method, as studies show that over 90% of employees receive wages this way, so you know that other small businesses already rely on it – and have for a while.

Keep records organized and available

Having payroll records organized and readily available is not only a good thing in case there are ever questions from your staff, but it can also be important to have them available should you ever get hit with an IRS audit. Because all of your payment records are housed and securely synced with your business and employee information, it creates a secure and comprehensive digital trail of payroll transactions (in case you ever need them).

Prevent security issues

Using direct deposit could help keep fraudsters from accessing your financial information as there won’t be paper checks with company information being physically transported around. This significantly decreases the chances that sensitive information could end up in the wrong hands.

Additionally, using a reputable payroll provider will offer robust security features, like end-to-end encryption, user access controls, firewalls, and server backups to ensure that your data stays safe and secure. Banks will have similar security features as well. This can give you peace of mind, knowing that your business and employee information is safe.

Less waste

Direct deposit could help employers save money by purchasing and printing fewer paper checks, as well as saving on the postage it takes to mail checks during each pay period. This might sound like a small savings, but for companies with a number of employees, the savings could add up significantly.

Employee advantages

Keep employee info and money safe

Both payroll providers and big banks offer a significant amount of security and protection. This includes end-to-end encryption, user access controls, firewalls, secure servers, data backups, and more.

Additionally, once the employee’s cash is in their bank account, it’s guaranteed by the Federal Deposit Insurance Corporation (FDIC). This US government agency insures money placed in banks, so if it’s lost for some reason, the US government will replace it (up to certain limits).

Time saved

It wasn’t too long ago that employees would have to travel to their financial institution and physically place their paper check into the hands of a teller who would literally put their money into their bank account. This is no longer a need since funds can be routed electronically, saving significant time and effort.

Less risk of loss

Workers no longer need to worry about misplacing a paper check or looking out for it in the mail, and similarly, they don’t have to worry about someone stealing it either out of their mailbox or out of their hands.

Fast access to funds

With direct deposit, employees may be able to access their money as soon as it’s deposited — often on the same day as payday. This is in contrast to paper checks, which employees have to wait for in the mail, and then drive to their financial institution in order to deposit the check and use the funds.

Is there any downside to direct deposit?

While direct deposit is an incredibly useful payroll tool, there are some potential downsides to keep in mind:

Cyber shenanigans

If you have ever received a spam email or phishing text, you’re likely aware there are some digital evil-doers afoot in this era of constant connectivity. And much like other industries, payroll scammers are always looking for ways to profit unscrupulously.

Payroll diversion scams are an example of this. In this type of scam, the scammer poses as a payroll authority or financial institution and sends an authoritative-sounding message to a target (either an employee or payroll personnel), asking them to change their direct deposit information. If the target believes that the message is legitimate and does what it says, then the funds would be diverted and sent to the fraudster instead of the employee.

Employees without accounts

Because fund transfers happen electronically, employees need to have a digital way — like a bank account — to receive funds. However, not all individuals have bank accounts for various reasons. As a result, you’ll need to exclude any employee who does not have a bank account from direct deposit during set-up. Instead, you’ll need to pay them using another method, such as cash or a prepaid debit card.

Costs

Though it is more than likely that an employer will end up paying less in postage and paper, there are fees associated with putting the direct deposit payment method in place. It could be a good idea to consider it as an investment, as you’ll save time on both payroll disputes, managing lost or stolen checks, and the administrative cost of distributing checks by hand.

How much does direct deposit cost for employees?

There’s no cost for employees when employers use this payment type. We point this out because it’s a detail your employees may ask about.

Setting up direct deposit is doable

Using direct deposit in your organization has benefits for both employers and employees. On one hand, employees can count on a seamless transfer of funds that is secure, reliable, and fast. Employers get peace of mind knowing that they have a reliable method that uses fewer resources, minimizes paycheck disputes, and that payday is taken care of.

Take a tour to see how easy payroll can be.

Jon Davis is the Sr. Content Marketing Manager at OnPay. He has over 15 years of experience writing for small and growing businesses. Jon lives and works in Atlanta.