More from our experts

If you’re operating a small business with more than one employee who works more than 20 weeks per year, you’re most likely required to pay payroll taxes as part of the Federal Unemployment Tax Act (also commonly known as FUTA).

And you’ll also need to prepare and file IRS Form 940, the Employer’s Annual Federal Unemployment Tax Return, each year.

Fast facts about Form 940

- Employers use Form 940 to report their Federal Unemployment Tax Act (FUTA) tax liability.

- Form 940 needs to be filed annually by employers if they paid wages of $1,500 or more in any quarter of a calendar year, or if they had one or more employees working for 20 or more different weeks.

- The due date to file Form 940 is January 31st of the year following the calendar year being reported.

- Filing late? Employers can be subject a penalty of 5% of the unpaid tax for each month — or partial month — the form is late up to a maximum of 25% of the unpaid tax.

Seem complicated? We’ve got your back with a quick explanation of how 940s work, a PDF download below, plus some guidance and instructions for completing yours.

Form 940 – Downloadable PDF

Above is a fillable PDF version of Form 940 that you can print or download.

What is Form 940?

Form 940 is an annual tax form that documents your company’s contributions to federal unemployment taxes. It’s based on the Federal Unemployment Tax Act (FUTA), a federal law that requires employers to pay taxes that cover unemployment payments for workers who lose their jobs.

Most employers are required to pay taxes under FUTA, so if you’ve paid an employee for more than 20 weeks during the year and their wages are more than $1,500 in a quarter, you will need to pay the tax and file your 940 return.

For agricultural employers, the rules are a bit different. You’ll also need to pay federal unemployment taxes if you:

- Paid cash wages of $20,000 or more to farmworkers during any calendar quarter, OR

- Employed 10 paid more farmworkers during some part of the day (whether or not at the same time) during any 20 or more different weeks

For businesses in most states, the effective tax rate is 0.06% (6% minus a 5.4% credit) of the first $7,000 in wages paid to an employee in a calendar year. Some states have lower credit amounts, so check the Department of Labor (DOL)’s website to make sure you’re using the right credit amount. Unlike most other payroll taxes, FUTA taxes are the sole responsibility of the employer and are not deducted from the employee’s paycheck.

Though a 940 is filed annually, employers are responsible for depositing taxes owed on a quarterly basis, with all deposits made using electronic funds transfer (EFT). If your business is new and you haven’t filed your first 940 yet, the IRS will automatically enroll you when you apply for your EIN. Don’t forget, most employers are also required to pay state unemployment tax (SUTA).

Who must file IRS Form 940?

Most employers are required to file Form 940, and determining whether you must file hinges on two factors: wages paid and number of weeks employees work. Each of these factors has a threshold: $1,500 and 1+ employees working 20+ weeks.

Let’s break down these two thresholds in a little more detail with this cheat sheet:

| The wages threshold | The work threshold |

| Form 940 must be filed if… | Form 940 must be filed if… |

| Your business paid wages of $1,500 or more to employees during any quarter. | You had one or more employees working for at least 20 different weeks during the year. |

| Note that these thresholds are “or” thresholds, not “and” thresholds. That means that if either of them are true in a calendar year, then you must file Form 940. | |

If you employ farm workers, then these thresholds are similar but slightly different. You must file Form 940 if you paid cash wages of $20,000 or more during the year, or if you employed 10 or more paid farm workers for at least 20 different weeks during the year. As you can see, the rules are less stringent for farm employs, which lowers the reporting burden for employers in the farming industry.

Who is exempt from filing Form 940?

A few different types of employers are totally exempt from filing Form 940, and others are simply below the above thresholds. Employers who do not have to file Form 940 include nonprofit organizations, government entities, and some other employers under certain circumstances. Let’s explore these exempt entities below:

- Nonprofit organizations with 501(c)(3) tax-exempt status are exempt from filing Form 940. This includes most of the nonprofits you know and love, like charitable organizations, religious groups, and educational institutions. However, if a nonprofit has unrelated business income that exceeds certain thresholds, they may be required to pay FUTA taxes and file Form 940.

- Government entities like federal, state, and local government agencies are generally exempt from filing Form 940. This includes public schools, public libraries, public services like police, medics, & firefighters, and other government-funded institutions.

- Other entities, such as railroad companies and certain household employers, such as those who hire nannies, babysitters, cleaners, gardeners, and other similar household employees.

Though a 940 is filed annually, employers are responsible for depositing taxes owed on a quarterly basis, with all deposits made using electronic funds transfer (EFT). If your business is new and you haven’t filed your first 940 yet, the IRS will automatically enroll you when you apply for your EIN. Don’t forget, most employers are also required to pay state unemployment tax (SUTA).

When should Form 940 be filed?

The deadline to file your 940 form is January 31 each calendar year. If your business has closed, or you stopped paying wages, you are still required to file a final 940, notifying the IRS about the change in status.

If you use modern payroll software or a payroll service provider, your 940 will likely be completed for you automatically. Remember, as the business owner, it’s still your responsibility to ensure that any deposits are made on or before the due date and that your return is accurate.

Beware: Quarterly tax payments

While your business only has to file Form 940 once a year, it probably needs to make quarterly FUTA tax payments. Any business that owes more than $500 in FUTA taxes should use the Electronic Federal Tax Payment System to submit quarterly payments by the end of April, July, October, and January. And keep tabs on those payments to make sure everything adds up at the end of the year.

Credit reduction states

An item to note for 2023 (and important to keep in mind when completing Form 940) is that the states of California and New York currently all have overdue unemployment insurance loans. While Uncle Sam keeps an eye out for these overdue payments — and because the loans are past due — each has been assessed a FUTA credit reduction for 2023 and has lost part of the 5.4% tax credit. For 2024, the DOL lists California, Connecticut, and New York as potential credit reduction states.

What does this mean for employers in these states?

Employers in California and New York will have higher payroll costs for 2023 as the new FUTA tax credit rate is reduced by 0.6%, lowering it from 5.4% to 4.8%. This means that the effective FUTA tax rate is 0.12% (up 0.6% from the standard rate of 0.6%). The potential 2024 credit reductions for these states (plus Connecticut) is 0.9%.

If you’re a business owner in one of the states mentioned above and unsure how to address your obligations as a result of the credit reduction (or how to account for it on Form 940), it’s a good idea to reach out to your accountant or tax professional to understand the implications for your company.

What do you need to fill out Form 940?

To complete Form 940, you’ll need the following:

- Form 940 – Downloadable PDF

- To know whether you’re required to pay state unemployment tax

- Experience rates (which help set your unemployment tax rate) for any state that you’re required to pay taxes in

- If your state is subject to a credit reduction based on money borrowed from the federal government

- Total amount of payments made to all employees throughout the year including compensation, fringe benefits, retirement and pensions, tips, or other payments

- Payment exemptions such as insurance plan contributions, group-term life insurance, dependent care, and other non-cash payments

- Total wages (if any) paid in excess of $7,000

Instructions for completing Form 940

There are currently seven parts that need to be completed for a 940. Here are the line by line instructions:

Form 940, Part 1

- In this section, indicate whether you had to pay state unemployment insurance in one (or more) states.

Line 1a. If your business has to pay state unemployment tax, enter the state abbreviation on line 1a

Line 1b. If your business has to pay state unemployment tax in more than one state, you will need to check the box on line 1b and complete Schedule A.

Line 2. If you paid wages in a state that is subject to credit reduction, which means it owes money to the federal government, check the box on line 2. For employers in states* subject to a credit reduction, you may owe additional federal unemployment tax. To figure out the amount, complete Schedule A of Form 940.

*In 2022, these states include California, Connecticut, Illinois, and New York.

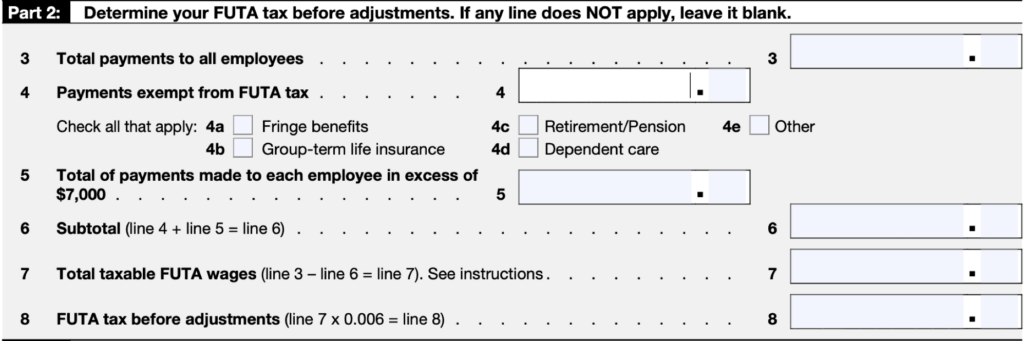

Form 940, Part 2

- Prior to any adjustments, you will figure our your FUTA tax in this section.

Line 3. Enter the total amount of payments made to all employees on this line

Line 4. Enter any payments exempt from FUTA tax, checking the corresponding boxes for exemptions such as fringe benefits, group-term life insurance, retirement and pension, and dependent care

Line 5. Enter the total amount of payments made to employees in excess of $7,000 (sometimes to referred to as excess wages)

Line 6. Enter the total of line 4 and line 5

Line 7. Enter the total taxable FUTA wages by subtracting line 3 from line 6

Line 8. Enter the total FUTA tax before adjustments on this line

Form 940, Part 3

- This section accounts for any adjustments that need to be made in the case that you are not receiving the full 5.4% FUTA tax credit.

Line 9. If ALL of the taxable FUTA wages you paid were excluded from state unemployment tax, multiply line 7 by 0.054 (line 7 × 0.054 = line 9) and go to line 12

Line 10. If SOME of the taxable FUTA wages you paid were excluded from state unemployment tax, OR you paid ANY state unemployment tax late (after the due date for filing Form 940), complete the worksheet in the instructions. Enter the amount from line 7 of the worksheet

Line 11. If a credit reduction applies, enter the total from Schedule A

Form 940, Part 4

- This section is used to calculate your FUTA tax balance that is due or overpayment (if applicable).

Line 12. Enter Total FUTA Tax after adjustments by adding lines 8, 9, 10, and 11

Line 13. Enter the amount of FUTA tax that has been deposited during the year, including any overpayment applied from a prior year

Line 14. Enter any balance due. If line 12 is more than line 13, enter the excess on line 14

- If line 14 is more than $500, you must deposit your tax

- If line 14 is $500 or less, you may pay with this return

Line 15. Here is where you enter any overpayment, with the option to have the overpayment applied to the next return or request a refund

Form 940, Part 5

- Use this section to report your FUTA tax liability by quarter ONLY if the amount entered in line 12 exceeds $500.

Line 16. Lines 16a, b, c, and d are where you will report your FUTA tax liability for each quarter

Line 17. This is the total liability for all four quarters

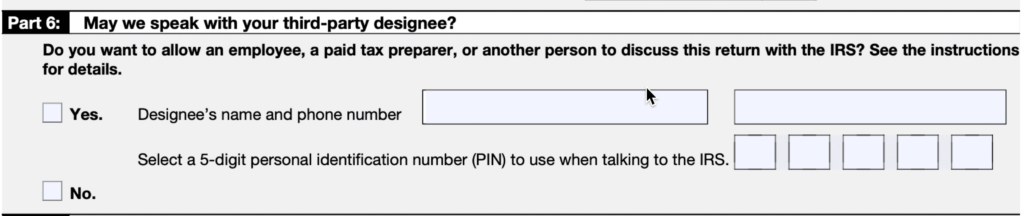

Form 940, Part 6

- Choose a third-party designee

Here you can designate (and give permission) to an employee, paid tax preparer, or another person to speak with the IRS regarding the FUTA return by simply checking the “Yes” box and adding the person’s name and contact information. The choice is yours and if you prefer not to, check off the “No” box.

If you check “Yes” in this section, make sure to include a 5-digit personal identification number that the designee can use to identify themselves as the third-party authorized to discuss Form 940 with the IRS. The pin number can be any combination of five digits you choose.

Form 940, Part 7

Sign and date the form.

Now that you have the form complete, you have options to make sure Uncle Sam receives it.

Can I file form 940 electronically?

Yes, Form 940 can be filed electronically (and FUTA taxes can be paid electronically too). You can file Form 940 online using an authorized e-file provider. Visit the IRS’ website to learn more about e-filing Form 940 and view a list of e-file providers authorized by the IRS.

Where do you mail form 940?

If e-filing isn’t your style and you’d like to mail Form 940 to the IRS instead, then keep in mind that the mailing address for paper filings depends on your location. You can find the right mailing address for you on Page 4 of the Form 940 instructions.

Find out more about Form 940

Now that you have more information about how to complete Form 940 and its purpose, let’s cover some other details that employers tend to ask about.

What is the difference between Form 940 and Form 944?

Both forms deal with reporting and paying unemployment taxes, but they serve slightly different purposes. Form 940 reports and pays FUTA tax on a quarterly basis, while Form 944 reports FUTA tax as well as the federal income tax withholding (FWT) for employers who elected the monthly deposit program. Form 944 basically combines the FUTA tax with income tax to simplify withholdings and reduce how often employers need to make tax payments.

What is the difference between Form 941 and Form 940?

While Form 940 and Form 944 deal with the same tax in different ways, Form 940 and Form 941 deal with different tax types altogether. Form 940 reports Federal Unemployment Tax Act (FUTA) taxes, while Form 941 reports Federal Insurance Contributions Act (FICA) taxes. These include Social Security and Medicare taxes, which are paid 50% by employers and 50% by employees. Form 941 is filed quarterly and FICA taxes are due quarterly.

How often do you pay 940 tax?

FUTA taxes must be paid quarterly by most employers, although Form 940 is only filed annually, on January 31st of the year following the year being reported on. FUTS taxes are due by the following quarterly deadlines:

- 1st quarter (January to March): due by April 30th.

- 2nd quarter (April to June): due by July 31st.

- 3rd quarter (July to September): due by October 31st.

- 4th quarter (October to December): due by January 31st of the following year.

And that’s it!

While your Form 940 is filed annually, please don’t forget about those quarterly FUTA tax payments. As with many other required employment taxes, a payroll service provider can easily automate payments and the form submission. We also recommend talking to a trusted tax pro if you have any questions.

You can also learn more about FUTA, in our detailed guide: What is the FUTA Tax? For more information on Form 940, visit the IRS website.

Take a tour to see how easy payroll can be.

Erin Ellison is the former Content Marketing Manager for OnPay. She has more than 15 years of writing experience, is a former small business owner, and has managed payroll, scheduling, and HR for more than 75 employees. She lives and works in Atlanta.