More from our experts

Businesses are taking notice of ICHRA as a premium reimbursement option as healthcare costs in the United States continue to rise. However, there are other reasons why this type of option, also known as an individual coverage health reimbursement arrangement, is gaining popularity with employers who use benefits to attract and retain employees.

OnPay’s research found that health insurance benefits continue to appear at the top of employee wish lists. However, getting all employees to agree on what should be included in a group plan can take time away from other things that businesses could be doing to move the needle forward.

To satisfy both employers and employees, using ICHRA as an option may be a good fit. This is because it allows employees to purchase plans that best suit their needs, while freeing up business owners to focus on their bottom line.

Fast facts about ICHRA options

- Allows employers to provide tax-free dollars to employees when they shop the marketplace for health coverage that fits their needs

- Came into existence when it passed Congress in 2020

- ICHRAs are a viable alternative to traditional group health coverage

Some data suggests that roughly 800,000 employers are considering using an ICHRA in the next five to ten years. But what is an ICHRA, how does offering one work, and what are employers responsible for once an employee buys the coverage they want? In this guide, we’ll talk more about some pros and cons and how ICHRAs can make sense for both employers and their employees.

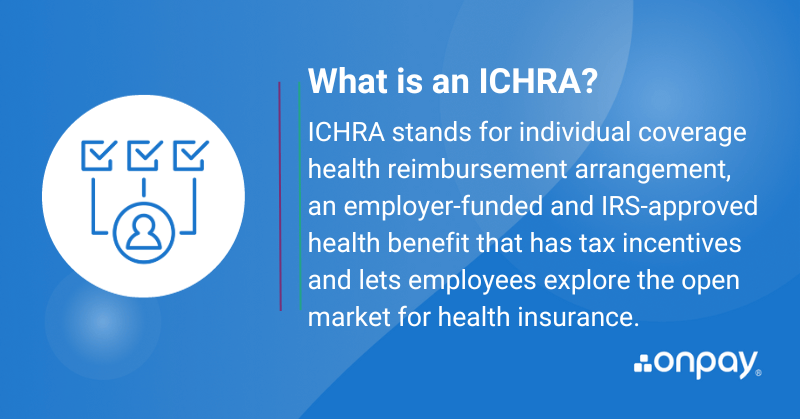

What does ICHRA stand for?

ICHRA stands for individual coverage health reimbursement arrangement, an employer-funded and IRS-approved health benefit that has tax incentives and lets employees explore the open market for health insurance.

Who can offer ICHRA as an insurance option?

Introduced in 2020, an ICHRA allows employers of almost any size to reimburse employees for some, or all, of the individual health insurance premiums for plans that they purchase on their own. To offer an ICHRA, you’ll need to have at least one W-2 employee on the payroll.

Instead of choosing a group plan, the employer agrees to cover a portion of the costs of the insurance that the employee chooses as being the best fit for their individual needs. For example, an employee could use a site such as healthcare.gov to search for plans, compare quotes, and make a purchase. This takes the guesswork out of an employer trying to find coverage that satisfies all of the employee’s needs. That said, where an employee shops for coverage is going to depend on the income an individual earns per year, their age, and the type of coverage they are looking for. Let’s explain a bit more about what we mean:

- If your employee earns less than $44,000 as a single person, Uncle Sam is going to provide a subsidy. In this case, the employee should use healthcare.gov

- On the other hand, let’s say this employee earns more than $100,000 per year. This employee is not going to receive a subsidy, they may be better off with a site like healthsherpa.com

The takeaway is that if an employee doesn’t qualify for a subsidy, there’s no reason to buy health insurance from the marketplace. You can use a site such as eHealthInsurance or Take Command Health. These are third-party administrators (also known as TPAs) that will help you set up an ICHRA.

Next, we will go over how to set up ICHRA as an option and how TPAs fit into the picture.

Double-dipping is not an option

With an ICHRA, employees can’t get a subsidy from the government AND reimbursement from their employer.

How does an employer set up an ICHRA?

Although employers can set up an ICHRA on their own, the vast majority work with a TPA because it is a complex process. Part of the TPA’s job is to act as a go-between you and your employees.

To learn more, we caught up with Paul Foery, the former Vice President of Insurance at OnPay, who is a benefits expert with more than 30 years of experience advising small businesses. He explains that using a TPA saves time and can prevent headaches. “The reason most employers choose to work with a third-party administrator is to take care of the heavy lifting and educate employees on how ICHRA works,” he says. “Employers ask the TPA to design the ICHRA based on their specific wants and needs, and create a plan document that spells everything out.”

In addition, there are tax considerations to think about, and TPAs can help with recordkeeping. “You need someone to keep track and have all these numbers together come tax time,” says Foery. “You can do this yourself with software — or work with a TPA. In many cases, they do charge an annual service fee.”

“The reason most employers choose to work with a third-party administrator is to take care of the heavy lifting and educate employees on how ICHRA works.”

— Paul Foery, former Vice President of Insurance at OnPay

Setting up an ICHRA with the help of a TPA

Here’s a high-level overview of how to get started with an ICHRA with the help of a TPA.

Dollars and cents

Since you will be reimbursing your employees using an ICHRA once they make their purchase, one of the first steps is to decide how much you are going to reimburse your team members. How much can you afford to reimburse employees? “Generally, a TPA interviews you and helps you decide how much money you want to give to your employees,” says Foery.

Plan document

The TPA sets up a plan document that spells out all of the rules, limits on reimbursements, and which employee classes are eligible. Keep in mind that the same rules must apply to all workers within a given employee class. However, you can increase reimbursements for older employees and those with more dependents.

Administer the plan

The TPA takes care of the legwork to set up the program. When it is set up, employees must have up to 90 days to choose their own individual plan. Your TPA should know this already, but:

- Annually, employers issue a notice (and once a year, they can decide whether to raise or lower the amount)

- The notice is sent to employees at least 90 days before the effective date of coverage through an ICHRA. The notice must explain how an ICHRA works with the reimbursement

Communication

The TPA communicates the rules of how the plan works to all of your employees (for example, through a company-wide email). If there are different employee classes with different plan details, the TPA takes care of communicating this information, so that everyone is on the same page, and knows the steps they need to take to obtain coverage.

For example:

“Hey, Company XYZ employees! To give you more choice in how your healthcare coverage works, the Company XYZ management team has set up an ICHRA so that you can shop around for a plan.”

“You now have 90 days to find a health insurance plan, and the employer is going to reimburse you for a portion of it. Please review the attached plan document to see how this works.”

“If you have any questions, reach out to us at Benefits XYZwe’re administering the ICHRA on behalf of XYZ. Here’s our email, phone number, and main point of contact.”

Receipt and invoice collection

Once an employee chooses and begins paying for a plan, they need to provide receipts to the TPA on a regular basis. For example, they are likely going to get a monthly bill or invoice for the coverage they have chosen. The employer then receives a report at the end of the month from their TPA: here’s everything we reimbursed to the employees. They keep all the records in case there’s ever a question from an employer or employee.

Employee resource

Employees can reach out to the TPA for assistance and questions. The TPA ends up being the information source for the employee — checking local zip codes and providing different carriers.

The beauty is that this way, everything is documented, and the employee doesn’t have to declare the reimbursement as income. If you do not have an ICHRA plan document set up properly and you pay $300 a month to the employee for them to pay for health insurance — that dollar amount being reimbursed is considered income. The amount needs to be added to the employee’s W-2, and he or she must pay tax on that.

“That’s why the ICHRA was created,” explains Foery. “It’s so you can have the money flow to the employee tax-free and give employers an option to do this legally. As an employer, this is an advantage of the ICHRA.”

Can a business offer an ICHRA and a group plan?

For larger employers, such as 600 employees or more, you can have an ICHRA and group plan coexist. Here are some things to consider.

You don’t have to pick a plan that everyone must use — if everyone doesn’t want the group plan, they can use the ICHRA option. For example:

- Those employees in class number one could be the workers in the warehouse — they have 90 days to pick a plan

- Those employees in class two — these could be your salaried employees on the group plan, and theyget set up the other way

-

- Employers don’t pay for plans that don’t get used

- It’s easier for you to budget — if you have 10 people and give each $300, the budget is $3,000

- With a group plan, you could have participation issues. Even if the employer pays half and nobody joins, it likely won’t get approval from a carrier. The carrier states that to create a group plan, you need to have a certain number of people on it

- Keep in mind that this is dependent on having a carrier or insurance company that will allow this type of arrangement

ICHRA is one or the other

Remember that employers are unable to give the employee the option of using both plans. Employees are not able to participate in both an ICHRA and a group plan. They have to choose one or the other.

“ICHRAs are becoming more commonplace as employers are choosing not to determine what health benefits should be anymore,” Foery explains. “For many companies, especially ones with a diverse staff with various health needs, employees can get frustrated no matter the plan that’s chosen.”

Employers put more of the decision-making process in the hands of employees by offering an ICHRA, rather than trying to accommodate every request for what people want in a healthcare plan.

“With an ICHRA, the business owner is no longer responsible for picking the health plan,” says Foery. “With this arrangement, the employee researches the marketplace to buy the plan that makes them happy.”

“With an ICHRA, the business owner is no longer responsible for picking the health plan. With this arrangement, the employee researches the marketplace to buy the plan that makes them happy.”

— Paul Foery, former Vice President of Insurance at OnPay

ICHRA example

Let’s say there’s a husband and wife who are both 32 years old, have three kids, and are thinking about having another. They likely have doctor’s office visits every week and may be willing to pay a little more to have a better plan with a lower deductible and a less expensive office visit co-pay. They have more choices, and that’s where an ICHRA comes in.

“The key takeaway is that each employee’s healthcare needs are different. Some are willing to pay a higher premium for better benefits, while others may not,” says Foery. In the past, everyone was boxed into the same plan. “With an ICHRA, each person is free to decide the best plan for their needs.”

In the end, the employer agrees to help with the costs of the employee’s healthcare without making the choice for them — the employee is able to choose and buy a plan on their own. “With ICHRA as an option, the employer now provides a nontaxable amount toward the cost of the plan,” says Foery. “Whatever the employee decides to buy, the employer can agree to provide a predetermined amount of money toward it.”

For example, the employer can decide to give the employee $1,000, $2,000, or whatever they choose toward the plan. With ICHRA, the employer no longer decides what the plan is going to be. “The marketplace is moving from a defined benefit to a defined contribution,” explains Foery. “This was not legal until ICHRAs were introduced.”

When an employer chooses to incorporate ICHRA into their benefits administration, it can reduce the administrative effort and potential frustration associated with finding a group plan that all employees can agree on.

Why do some employers offer ICHRA plans?

ICHRAs can provide beneficial flexibility. In addition to giving employees the ability to choose their provider, offering individual health insurance coverage can help employers spend less time trying to find a health plan that all of their employees can agree on.

ICHRA pros and cons

Offering an ICHRA health reimbursement plan can have benefits for both the employer and the employee. Once more, we spoke with Foery, who says that this type of arrangement can help with what has traditionally been a balancing act of understanding what each employee wants (and expects) from their health coverage. “There can be different advantages to offering an ICHRA,” says Foery. “First, it gives employees more choice since they can research the marketplace and find a plan that suits their personal needs best.”

Foery points out this helps mitigate some of the hassles of trying to fulfill each employee’s needs. “ICHRAs can reduce some of the legwork employers typically go through trying to satisfy what everybody on staff expects from a group plan.”

It can also make sense if there’s not enough employees who will participate.

“If an owner is unable to meet participation requirements (maybe you only have 3 out of 10 employees who want to participate), you are not going to be eligible for a group plan,” Foery says. “So, an ICHRA could be a good solution for those companies with smaller teams.”

Some ICHRA pros that can make sense for employers

- Individual health insurance plans allow businesses to reimburse employees for health insurance premiums they purchase on their own. Employees have more options because they can shop the marketplace for the best plan for their needs.

- If you like, you’re able to separate by employee class, which can help with budgeting since you can provide different monthly allowances to each class. Offering a different monthly allowance to different classes of employees can also help you better prioritize and plan your health benefits budget. Do you have 50 or more employees? Keep in mind that you’re required to offer access to health coverage since you would be considered an applicable large employer (ALE) per the Affordable Care Act (ACA). The good news is that if you are considering ICHRA, these plans do fall under the ACA’s mandate.

- In the long term, ICHRAs can be less expensive for businesses than providing a group health plan, especially for small businesses or businesses with part-time or seasonal employees. This is because a business can set a defined contribution amount per employee.

Potential ICHRA cons worth knowing

Now that we have covered some of the benefits, let us look at some of the potential drawbacks.

- There’s a loss of group buying power because these are individual plans that employees buy. The same group purchasing benefits as traditional group health plans generally don’t exist. This means premiums may be higher.

- There is a learning curve — as we mentioned, ICHRAs are relatively new. Employers will really need to understand the “ins and outs” to clearly communicate benefits for employees. Remember that the burden of research is put back on the employee (that’s why employers will seek out a TPA).

- Age-banded premiums — older employees could end up paying higher premiums for individual plans purchased through an ICHRA.

- People cannot “double-dip” — it’s one plan or the other.

Does each employee receive the same amount of money towards an ICHRA?

As we mentioned earlier in the article, ICHRAs should provide more flexibility and can generally offer different reimbursement amounts to different classes of employees. Keep in mind that the classes must be defined to avoid discriminating against anyone based on health factors. What does this mean? Below are some examples of classes that are typically acceptable.

- Full-time employees vs. part-time employees

- Salaried employees vs. hourly employees

- Employees working in different geographic locations

- Workers that have different job duties or titles

- New hires that joined your team in the past year, versus employees with longer tenures

The classes above are also referenced on page 20 of the Federal Register.

For example, an employer could offer the following ICHRA structure, using a monthly allowance:

- Full-time salaried employees: $300/month reimbursement

- Full-time hourly employees: $200/month reimbursement

- Part-time employees: $100/month reimbursement

As you can see, the employer gets to define the classes, determine appropriate reimbursement amounts for each, and set different caps on how much is available to employees in each class.

It is worth mentioning again that the key here is that the classifications must be based on employment-related criteria: discrimination based on health factors is a no-no and should be avoided. All employees within a class must receive the same offer of benefits.

ICHRA is another option for employers

Various strategies are used to attract and retain top-tier job candidates and employees, but providing health insurance is usually a key piece of the puzzle. ICHRA might be worth a closer look if it is becoming difficult to get everyone on the same page about health coverage.

Because these types of plans give employees more say in the type of coverage they receive and can take a time-consuming task off the plate of employers, ICHRAs could be a “win-win” depending on your company’s goals. Best of luck as you compare options on the market — our team is always available to answer any questions!

Take a tour to see how easy payroll can be.

Jon Davis is the Sr. Content Marketing Manager at OnPay. He has over 15 years of experience writing for small and growing businesses. Jon lives and works in Atlanta.